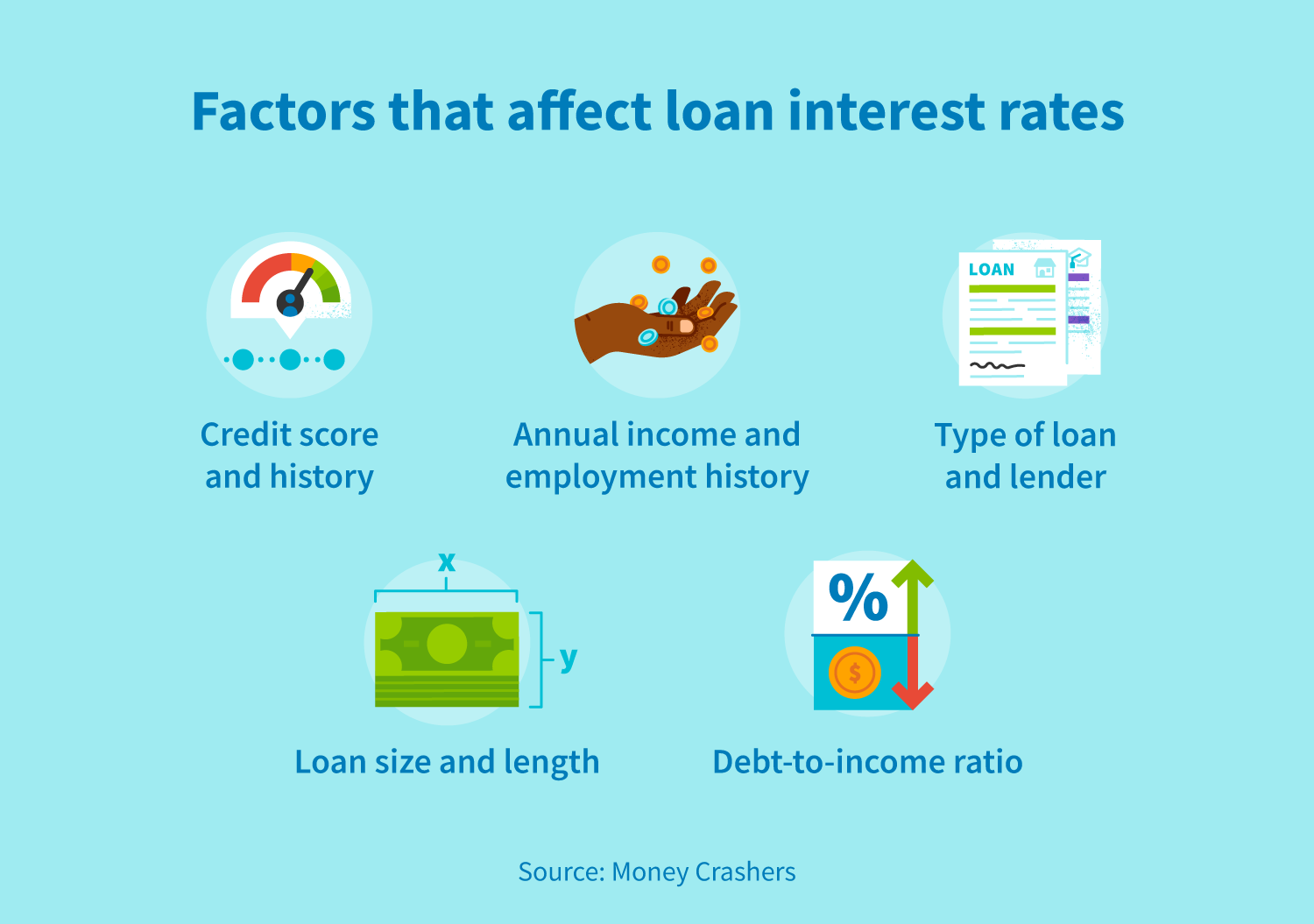

Another person’s financial obligation-to-earnings proportion is a helpful shape when choosing whether or not they is undertake even more obligations and repay it effortlessly. So it proportion works out the brand new borrower’s money facing the complete debt burden. The brand new proportion is actually conveyed inside percent, additionally the FHA advice claim that the utmost debt-to-earnings proportion having individuals should not be any more . This means that one’s monthly home loan should not be any more than 30 percent of your own salary, while you are the complete month-to-month debt burden (mortgage payments, handmade cards, car loan, student loan payments, etc.) doesn’t meet or exceed 41 percent of monthly income.

You can find, yet not, instances when exceptions are built, including times in which highest down payments are built, or even the debtor provides advanced level borrowing from the bank, higher cash supplies Harpersville loans, and other points that will allow them to take on extra financial obligation easily. Observe that bills particularly cable costs, web sites charges, fitness center memberships, utility bills, etc., dont amount as part of the 43% restrict, while they is actually charged regularly.

The house or property Assessment Process

The process would-be quite the same as what goes on when you to applies having conventional financing, into the important difference becoming your FHA possesses its own appraisal agents.

Appraisals need occur when obtaining home financing if in case trying to practical refinancing or contrary mortgage loans. Another advantage off writing on the brand new FHA is they carry out n’t need appraisals getting smooth refinancing. It must be noted that appraisals will vary at home inspections, being just used to make certain that a house fits brand new lowest coverage, livability, and you can hygienic requirements.

Household Equity Funds

Antique household security fund can be put to almost any make use of the debtor wishes. You’ll find, yet not, different varieties of financing programs which can be used some other intentions other than family instructions, including while making home improvements supported by the fresh new borrower’s family equity. They also promote seniors reverse mortgages. Such funds were:

Do-it-yourself Money

Brand new FHA 203(k) Loan was created to enable it to be consumers to get a single financing that will allow them to buy property and you will additionally create improvements and you can repairs. You are able in order to obtain according to research by the home’s speed while the price of repairs or the projected property value immediately following the brand new upgrades and you will fixes was over.

Even if the total price is higher than the fresh property’s well worth, you can do this. That it financing system can be drawn while the a form of cash-aside refinancing, whilst money will need to be directed for the do-it-yourself.

This new 203(k) will come in the streamlined and practical adaptation, where sleek program is initiated for much more small, non-architectural improvements and you may repairs. The standard version was created to helps far more thorough programs eg once the the fresh roof, including the latest rooms, structural fixes, or one services that cost more than simply $thirty-five,100000 and then have the very least loan worth of $5,100000.

Title We Finance

FHA Identity We funds resemble 203(k) money while they allow borrowers to obtain financial support getting renovations without the need to re-finance their financial totally. They arrive in the a fixed payment price lasting doing twenty years. Single-family unit members home features an upper financing limit out of $25,one hundred thousand.

not, you can not call this type of financing real home security financing as there are not any family equity otherwise collateral requirements having fund below $seven,five hundred. Such mortgage is present to individuals concentrating on rental properties otherwise are formulated (mobile) residential property.

Such finance are made to let individuals improve livability and you can utility of its homes, that may involve furnace installation, lesser repairs, window installation, insulation fitting, exterior completing, etcetera. ‘Luxury’ improvements, such as for example swimming pools or hot spa setting up, aren’t incorporated below so it umbrella. You will want to pose a question to your bank what exactly is and what is perhaps not welcome here just before entering the project.